Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Are You Serious About Investing? Then Read ThisBy

Wednesday, September 7, 2016

You can buy stocks like one of the world's most famously successful investors... if you just follow his blueprint.

To this day, Warren Buffett's success is legendary... And whether he's buying an entire business outright or simply purchasing shares of its common stock, the "Oracle of Omaha" says he has always taken the same approach.

Buffett employs a "bottom up" approach that looks closely at all aspects of a particular business, irrespective of things like employment levels, industrial production, or the direction of the stock market.

It all hinges on four simple tenets. These are the things that Buffett considers all-important. If you look for them, you can learn to buy stocks the Buffett way...

Tenet No. 1: Simple and Understandable

From Buffett's perspective, an investor's success is directly proportional to his understanding of the investment. This is one trait that separates investors who focus on the business from most hit-and-run investors.

You can't fully appreciate a company's opportunity tomorrow until you first understand what makes it tick today. The more complicated the business is now, the less likely you are to properly imagine how its story might change in the future.

Tenet No. 2: Favorable Long-Term Prospects

The great Wayne Gretzky famously said, "A good hockey player plays where the puck is. A great hockey player plays where the puck is going to be."

Over the arc of his investing career, Warren Buffett has done a masterful job of identifying businesses with favorable long-term prospects... of skating to where the puck is going, not necessarily where it is today.

A prime example is auto insurer GEICO, which was close to bankruptcy when Buffett started buying it 65 years ago. In his 2015 letter to shareholders, Buffett explained...

Tenet No. 3: Honest and Competent Management A business can only be as good as the people it attracts and retains. Buffett tests management's honesty and competency by asking three questions:

Tenet No. 4: Attractive Pricing The final step is to assess to what degree (if any) the current price represents a discount to the business' intrinsic value. The greater the difference between the two, the greater the margin of safety.

Buffett believes the best way to determine intrinsic value is a technique called discounted cash flow (DCF) analysis. You simply discount the net cash flows expected to occur over the life of the business by an appropriate rate. The resulting net present value (NPV) provides an estimate of the company's intrinsic value.

Most investors and analysts – Buffett included – prefer to discount projected future cash flows using a "risk free" rate. Normally, the 10-year U.S. government bond would be a reasonable point of comparison... but not when the Treasury-bond yield is as low as 2%, like it is now.

Because of this and the other shortcomings associated with DCF analysis, we prefer to take a more market-oriented approach to estimating intrinsic value. Over the years, we've observed that high-quality businesses with strong margins, balance sheets, and returns on equity often sell for 25 to 30 times free cash flow (i.e. operating cash flow less capital expenditures). That's why we're constantly on the lookout for quality businesses trading at or below 15 times FCF. Buying a business with an intrinsic value of 25 to 30 times FCF at or below 15 times FCF helps us capture a margin of safety similar to the one Buffett is looking for using DCF analysis.

In summary, Buffett keeps it simple. He stays within his circle of competency, happy to pass up businesses he doesn't fully understand and those for which he can't confidently predict future cash flows. He also spends just as much time evaluating management's words as he does the numbers they generate. Finally, he insists on buying quality businesses at prices that provide a substantial margin of safety – just in case he's wrong.

As you construct your own investment-selection model, I suggest you emulate the one Warren Buffett has used for more than half a century. It's the blueprint that helped him become the world's greatest investor.

Good investing,

Mike Barrett

Further Reading:

Read more of Mike's timeless wisdom on improving your investing skills here...

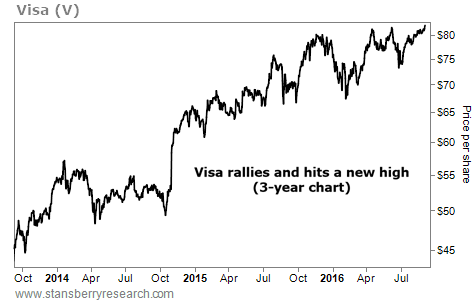

Market NotesTHE AMERICAN CONSUMER IS ALIVE AND WELL Today's chart is a good sign for the U.S. economy...

Regular readers know we enjoy keeping track of companies that tell us how much money American consumers are spending. And while things aren't completely healthy within the U.S. economy today, they aren't as bad as some people would have you believe.

For proof of that, we turn to Visa (V). With more than 2.5 billion Visa cards in use, the world's largest credit-card company handles more than 100 billion transactions per year. It takes a small percentage from each transaction, making the company's profits and share price a "real time" read on how much money is changing hands.

You can see in the chart below that Visa's shares just broke out to a new 52-week high. The stock is up 12% since late June... and more than 20% from its most recent low in early February. As long as people continue to use their credit cards, things can't be all that bad...

|

Recent Articles

|