Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Ten Attributes of Great Fundamental Investors, Part IIBy

Thursday, December 22, 2016

In yesterday's essay, I introduced you to Michael J. Mauboussin, a prominent value investor, author, and longtime adjunct professor at Columbia University.

Mauboussin estimates he has devoted two-thirds of his 30-year investing career to thinking and writing about the investment process. Last summer, he condensed those two decades of insights and analysis into an essay titled "Reflections on the 10 Attributes of Great Investors."

Yesterday, we reviewed five of those attributes. Today, we'll explore the remaining five...

The way we think and feel directly affects our investment behavior and "biases" our decision-making process. Robert P. Seawright, a successful money manager and author, considers what I've summarized below to be some of the most common behavioral biases for investors:

Mauboussin believes great investors are generally less affected by these behavioral biases because they acknowledge the existence of these biases, learning how to cope with them. They create a working (investing) environment that helps them "think well."

The late Amos Tversky was a brilliant mathematical psychologist and author of highly regarded works on behavioral economics. Philip E. Tetlock, in his excellent book, Superforecasting: The Art and Science of Prediction, recalls Tversky telling him that most people only have three probability settings: "gonna happen," "not gonna happen," and "maybe." If you aspire to investing greatness, this three-setting dial won't cut it. As Mauboussin says, superior returns come from constantly seeking an edge "where the price for an asset misrepresents either the probabilities or the outcomes."

Superforecasters – a group of ordinary folks who consistently out-forecasted their peers in the U.S. intelligence community – routinely demanded far greater granularity of themselves. The lesson they teach us is this: Your edge comes from digging so deeply into the problem at hand that you understand the finer-grained issues – and how they're likely to influence the outcome.

Mauboussin says great investors do two things that most of us do not: 1) They seek out information and/or views different from their own, and 2) they update their beliefs when the evidence suggests they should. As he puts it: "Beliefs are hypotheses to be tested, not treasures to be protected."

It's easy to forget that there are two aspects to superior returns: finding an edge, then exploiting it with proper position sizing. If you develop a strong conviction for a particular investment but don't size it accordingly, you're not maximizing the potential payoff from your edge. That's why, in Extreme Value, we recommend subscribers allocate higher proportions of capital to our highest-conviction picks.

Berkshire Hathaway's Charlie Munger says it best: "In my whole life, I have known no wise people (over a broad subject matter area) who didn't read all the time – none, zero." Many successful people make reading a priority. If you aspire to investing greatness, you should, too.

Every investor, novice or pro, should aspire to realize Mauboussin's 10 attributes. If you aspire to be a great fundamental investor, consider this your trusted playbook.

Good investing,

Mike Barrett

Further Reading:

Yesterday, Mike shared the first five attributes of great fundamental investors. Catch up on them here.

In August, Dan Ferris shared the one rule that virtually guarantees you to make money in the stock market over the long term. Ignoring this lesson could cost you a fortune. Read more here: A Timeless Rule Followed by Every Wealthy, Sophisticated Investor.

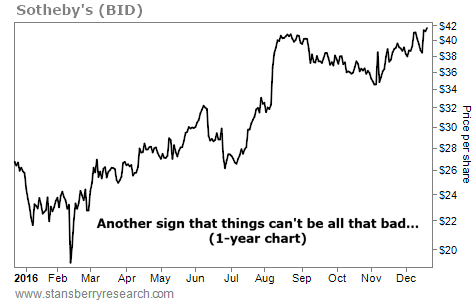

Market NotesANOTHER SIGN THAT THINGS CAN'T BE ALL THAT BAD Today, more proof that things aren't as bad as the talking heads on CNBC would lead you to believe...

Over the past few weeks, we've highlighted the share-price breakouts in companies that sell expensive trips and extravagant purchases. We can add high-priced art to the list... Last month, a 1902 painting by expressionist Edvard Munch sold for $55 million at auction.

That's great news for the bottom line of prestigious auctioneer Sotheby's (BID). The global art dealer recently reported more than $7.5 billion in aggregate sales in 2016.

As you can see in the chart below, that has been a boon for BID shares. The stock recently hit a fresh 52-week high and has more than doubled since February. When business is booming in the fine-art sector, it's a sign that things can't be all that bad for the U.S. economy...

|

Recent Articles

|