Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Follow These Two Rules to Hold on to Your Long-Term WinnersBy

Wednesday, January 25, 2017

Twenty-five years ago, a back-office snafu cost me $6,000. The worst part is, it didn't stop there...

I owned Oracle (ORCL) and Microsoft (MSFT) in my IRA, and both were sold out of my account. By the time I realized they were gone, the stocks had tripled.

I kicked myself for not catching the error earlier. That was mistake No. 1.

My second mistake was even costlier...

I consoled myself with the thought that the stocks had risen so much, they couldn't possibly go any higher.

And that mistake cost me $130,000.

Let me explain...

Microsoft went on to rise 3,000%... and Oracle grew by 9,900%.

In my early investing years, I missed out on other profits in similar ways. I would close out of stocks for quick 20%-30% gains... only to see shares rise tenfold in the following years, or even more. For me, those missed winners have always "hurt" more than losers.

After missing out on so many long-term winners, I became determined to learn a method that would help me hold on to them longer.

The key question I asked myself was this: How do you know which winners you should hold for the long haul and which winners you should sell quickly?

This question drove me to study the common traits of superstar stocks.

I examined hundreds of stock charts. But I couldn't find a common denominator on the technical side.

That meant there had to be a fundamental reason why these stocks would go up thousands of percent.

I had to find it...

Along my journey, I stumbled upon an investment book called Common Stocks and Uncommon Profits. Phil Fisher wrote it in 1958.

Fisher was a West Coast money manager with a fabulous track record. (His son, Ken Fisher, went on to become a billionaire money manager.) Phil Fisher had an uncanny knack for both buying and holding stocks that would turn into massive winners.

The most important thing I learned from Fisher came from a one-sentence passage in his book:

If the company is deliberately and consistently developing new sources of earning power, and if the industry is one promising to afford equal growth spurts in the future, the price-earnings ratio five or 10 years in the future is rather sure to be as much above that of the average stock as it is today.

There are two key takeaways from this one passage:

If the answer to both questions is yes, then you've found yourself a potential long-term winner... Let me give you an example of how these two rules work using a stock we own in the Palm Beach Letter portfolio.

We bought Nvidia (NVDA) back in December 2015. Subscribers who got in when we recommended the stock are now up nearly 218%.

As a younger hedge-fund manager, I might have sold out of NVDA by now to lock up some quick profits. But I'm in no hurry to sell it because it fits Phil Fisher's two rules.

Let me show you...

Nvidia started off making graphics cards for computer games. But over the years, Nvidia has expanded its revenue streams by making chips that enable artificial intelligence, autonomous driving, and cloud computing. Not only that... but Nvidia is making a push into the content-streaming space. It's about to launch a service that will let you play high-end PC games on a regular computer.

Nvidia estimates a potential 1 billion PC users would love to play computer games but can't because of cost. High-end gaming rigs cost more than $2,000. But streaming games brings the cost way down.

It's like borrowing your friend's top-of-the-line computer... only this machine lives in the "cloud." It works just like streaming a movie on Netflix, and the starting price is the same... $7.99 per month.

This new business could be even more lucrative for stockholders than when Netflix started out.

That's because the global PC gaming industry is twice the size of the movie industry. That's not a typo. The global PC gaming industry is bigger than the movie-streaming and traditional Hollywood box office industries.

This one business alone could be worth billions.

So, it's clear that Nvidia meets Fisher's first rule of creating new streams of future revenue.

Now, let's move on to his second rule...

Remember, Nvidia has grown from selling just graphics cards to now providing artificial intelligence, autonomous driving, cloud computing, and PC game streaming. As you look at each one of these industries, I don't think you need to be a rocket scientist to know that the demand for them is just getting started.

Based on Fisher's two criteria, NVDA could double in price again. All told, that will be a sevenfold increase from our original entry price. And that's why I won't sell it now.

So, if you want to hold on to long-term winners, and not sell them prematurely, remember these two simple questions:

Is the company developing new sources of earnings power?

Is the industry promising to afford equal growth spurts in the future?

By applying a little common sense, you can start using Fisher's timeless wisdom to uncover your own massive winners.

Regards,

Teeka Tiwari

Further Reading:

"Not all small companies become big companies," Chris Mayer writes. But after three years studying stocks that returned 100-to-1, he has found a few clues to their breakout success. Learn what the stock market's biggest winners have in common by reading here: Three Clues to Finding the Next 100-Bagger.

"In the end, you can't earn a dollar unless you have a business that consistently earns money," Dr. David Eifrig wrote recently. If you want incredible gains over the long term, these businesses deliver, no matter what the economy is doing. Read more here: Buy These Companies and Ignore the Noise.

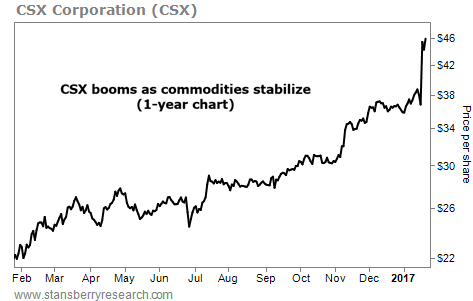

Market NotesTHIS INDUSTRIAL BUSINESS IS BOOMING Today's chart highlights a stock that's rising with commodity prices...

Over the past five years, the Bloomberg Commodity Index – which tracks a basket of commodities – fell 52%. The plunge was partly due to weakness in the coal market. But now, coal is stabilizing... For instance, metallurgical coal, used in iron and steel manufacturing, more than doubled in 2016.

The railroad business has been one of the biggest beneficiaries of stronger coal prices. Railroads transport 37% of all coal shipments in the U.S. each year. And nearly 70% of all coal shipped to power plants arrives by rail. You can see this trend in action with shares of CSX Corporation (CSX)...

CSX has been in a steady uptrend since the beginning of 2016. But last week, shares spiked 23% when activist investor Paul Hilal and the former CEO of Canadian Pacific Railway (CP) Hunter Harrison announced plans to take over the company. With commodity prices on the rise and an activist investor at the helm, look for CSX shares to continue higher...

|

Recent Articles

|