Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

The Weekend Edition is pulled from the daily Stansberry Digest. The Digest comes free with a subscription to any of our premium products.

The Real Trouble With 'Bizarro Capitalism'By

Saturday, July 22, 2017

To preview the conclusions, you'll find below there's a hidden downside to global central banks' campaigns of endless credit expansion and zero interest rates: As capital costs disappear, so do profit margins.

Equity investors will surely cheer financial innovations that lead to rapid amounts of revenue growth. But bond investors – those dreary troglodytes – focus on cash flows.

Trouble is, despite wondrous new products, massive investments in research and development, capital expenses (like plants and equipment), share buybacks, and gigantic acquisitions... most of America's top companies aren't producing additional cash flows. But they are producing a lot of new debts.

How will this end? That's the question I (Porter) will attempt to answer today.

(Truly refined readers will recall the Seinfeld episode "Bizarro Jerry," which adopted the same metaphor. Seinfeld's sometimes-girlfriend tells him she has picked a new man who is the polar opposite of him, "Bizarro Jerry.")

Bizarro Capitalism is my extension of these ideas. It means a system of exchange and property ownership where capital is free and therefore requires zero savings or profits to grow.

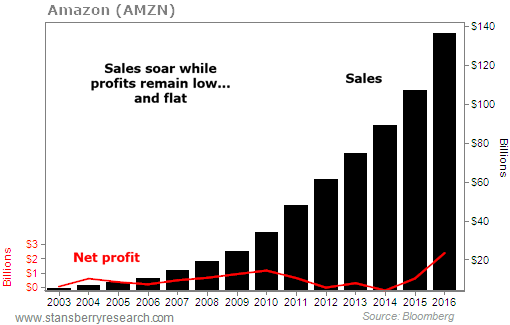

Here was a company that had grown tremendously. Since 2013, the online-retail giant's revenues soared from $80 billion to $140 billion annually. Those are huge numbers.

And profits? There aren't any in its consumer businesses. Its corporate-services business (Amazon Web Services) makes about $1 billion a year currently.

So over the last three years, on revenues of $320 billion, Amazon made about $3 billion in profit – or less than 1% of sales. Nevertheless, it had invested an incredible $17 billion on acquisitions and capital improvements – before its $13 billion acquisition of Whole Foods Market (WFM). In total, the company has now spent $30 billion on investments in its business... almost none of which are expected to make a profit.

Stocks in general have virtually never been this expensive before as measured by the ratio of share prices to revenues or profits. Bizarro leaders like Amazon and Netflix (NFLX) have seen their share prices explode.

When Amazon introduced the Kindle e-reader that gutted the profitability of every other book retailer, the stock was trading for around $90 per share. Roughly 10 years later, it trades for more than $1,000 per share – an increase of more than tenfold.

But Amazon wasn't just targeting book retailers. Even though online retailing today only makes up about 10% of retail sales, the price competition it has engendered makes it almost impossible to maintain a profit margin in the sector.

Finally, investors are beginning to realize the downside to Bizarro Capitalism. As you can see below, the retail sector looks like a war zone...

All these stocks, and many others, will likely go bankrupt. And the recovery rates on these bonds will not be normal (around $0.45 on the dollar) because no one is going to buy these companies or their assets beyond their inventories.

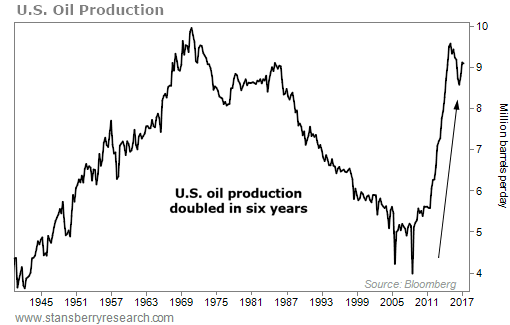

But the biggest problems from Bizarro Capitalism will occur in the commodity markets. Virtually free capital has led to a huge increase in commodity production, from oil to corn.

Since July 2011, U.S. onshore crude-oil production has essentially doubled. The last time U.S. crude-oil production doubled, it took 25 years, from World War II until the mid-1960s. We've done it again in just six years. Corn has seen a growth in production of almost 50% since 2012, from 10.8 billion bushels to 15.1 billion bushels.

Since Bizarro Capitalism doesn't require anyone to delay consumption (for savings), there's no pent-up demand for any of this stuff. Oil and corn demand have barely grown.

That's why prices have fallen so much. Bizarro Capitalism is a recipe for collapsing profit margins (like retail). But it's also a recipe for collapsing commodity prices. And that sounds good... until you understand more about how Bizarro Capitalism really works.

You see, even though the money doesn't come from savings, it still has to be borrowed. And the folks who lent all of this capital don't think of it as funny money. They think it's real. And they're going to want it back, with interest.

The tractor manufacturer had lent farmers $38 billion to buy tractors and other items necessary for farming. (That explains the huge increase to corn production.)

The Wall Street Journal noticed this, too. This week, it published a well-researched article, noting that John Deere had become the fifth-largest agricultural lender in the country...

Should one of America's most important manufacturing companies be inflating the demand for its products by becoming one of the largest agricultural banks in the world? Isn't it obvious that these loans are going to lead to far too many tractors being sold, sharply lower corn prices, and eventually, a new financial crisis in America's heartland?

Deere, like many manufacturers in this credit cycle, has used leasing, even more than lending, to sustain demand for its products. Since 2010, the value of Deere's outstanding leased equipment has soared, from less than $2 billion to almost $6 billion. The Journal explained...

Trouble is, when you provide leases for equipment that make them much cheaper to own, you make it much harder to earn a profit selling the same equipment. Deere has seen its profit margins on its equipment sales fall from $5 billion to less than $2 billion. That's Bizarro Capitalism: plenty of revenue, but no profit.

Eventually, all of those leased tractors get returned. If they can't be sold quickly, Deere takes the loss. Over the last three years, the amount of equipment leased out by Deere is up 87%. But what have corn prices done? Nothing. So... what do you think will happen next, after three years of booming lease business and no profits from farming?

The stock market couldn't care less about these risks. Shares of Deere have moved from around $75 to more than $120 in roughly the last year alone. And right now, the bond market couldn't care less, either. Deere's long-dated bond (the 5.375% bonds due in 2029) is trading for $24 over par ($124) and yielding 3%.

Will Deere successfully use virtually free money (in the form of endless supplies of credit) to prop up demand for its tractors forever? Will U.S. oil producers be able to lower their operating costs forever? (Recently, the average breakeven price for high-quality onshore production fell from around $50 to around $40, a change that has forestalled bankruptcy for a large number of U.S. oil producers.)

My bet is no. And like I first told Digest readers in April... sooner or later, the gigantic credit bubble that lies at the heart of Bizarro Capitalism will burst.

Of course, I can't give you a date to put on your calendar. But keep your eye on the market for high-yield debt. The credit market will see these problems coming long before the stock market does.

Today, you can hedge your entire equity portfolio with a small number of long-dated put options trading at dirt-cheap prices.

But that won't be the case forever... When the stock market finally wakes up to these problems, it will be too late. Volatility will return – practically overnight – and put-option prices will soar hundreds or even thousands of percent as investors panic.

In other words, the best time to buy "hurricane insurance" is when the sun is still shining. And you have that chance today.

This is exactly what we've shown readers in our Stansberry's Big Trade service. But we've taken this strategy one step further.

We've identified the weakest, most troubled companies in the market today, a list we've dubbed the "Dirty Thirty." Each company on the list is heavily indebted and has serious flaws in its business model.

These firms are likely to struggle even if the bull market continues longer than we expect... And they're absolutely doomed when the credit cycle finally rolls over.

If you're not already reading Stansberry's Big Trade, I urge you to take a closer look today. Click here to learn more.

Regards,

Porter Stansberry

|

Recent Articles

|