Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

How to Rescue Your Retirement in Four Easy StepsBy

Friday, October 20, 2017

Forget fear... Stress is the real hurdle for retirement savings.

According to a recent survey run by Schwab Retirement Plan Services, day-to-day financial stresses keep folks from contributing to retirement plans.

The biggest issue? Debt. In fact, Americans today owe more than they did in December 2007, just as the recession started. It's a common reason folks don't invest for retirement.

Here's what's even more worrisome... Those surveyed said they spend more time choosing which car to buy than they do planning their 401(k) investments.

We can't rely on pensions anymore. You need to grow the wealth on your own... And you'd better spend more than a second choosing your investments. That new car might last you a decade or two, but we're talking about setting yourself up for the rest of your life...

"I'll start saving after I pay off my credit-card debt... after the kids are done with school... after I get that new job... after the next market correction... "

If any of these sound familiar, you're shooting yourself in the foot. As we've written before many times... the sooner you start saving for retirement, the better.

Think about it this way. Imagine you save $5,000 a year for 40 years and earn just 4% a year on your investments... You set aside $200,000, and it grows to $494,000. But if you boost your annual return to 8%, the same $200,000 grows to $1.3 million.

By the way, we didn't pick these numbers at random. A study by research firm DALBAR shows that while the stock market earned about 11.1% a year over the last 30 years, the typical investor only earned about 3.7%... thanks to bad investment decisions. (We decided to use a more conservative market return of 8% a year.)

And in the new era of 401(k)s and IRAs, the investment performance falls on you. Getting just 4% won't cut it. You owe it to yourself and your family to earn the best return possible.

So here are four easy steps anyone can take to get in a stronger financial position today...

1. Make a budget.

List out all sources of income, all your fixed monthly bills (like your mortgage, utilities, and insurance), and all your variable bills (things like entertainment, dining out, vacations, etc.). Getting a full picture of what comes in and what goes out will help you make adjustments for step two.

2. Save, save, and save.

The more you can save (and sooner), the better off you'll be in the long term. We ran the numbers on the average American saving 5% of his income... With a modest investment return of 5%, it will take 65 years to accumulate enough wealth to replace his income without touching the principal.

Bumping up your savings to 10% would lower that to 50 years... And sacking away 30% takes it down to 30 years. When you add to this the power of compounding over time, the earlier you start saving more, the better your future.

3. Do your homework.

The multitude of offerings in a traditional 401(k) or IRA is enough to overwhelm anyone.

Typically, I like to start with a simple allocation: Decide between stocks and bonds. If you have a longer-term view and a higher tolerance for risk, you might make your allocation 80% stocks and 20% bonds. If you are closer to retirement and don't like volatile returns, you could do 70% bonds and 30% stocks.

But more than anything else, you'll need to fully understand all of the associated fees with each investment. Don't throw away money on management and other fees that you could avoid by choosing a different vehicle. One percent here, two percent there can all add up to a huge chunk of your money.

4. Make use of employer matching and catch-up contributions. Employers may match contributions to your retirement accounts. Find out if they do, and take full advantage of the matching program. Here at our company, we match up to the first 6%.

Catch-up contributions will help make up for lower contributions early in life. Once you hit 50, you can start increasing your contributions to IRAs, 401(k)s, and other accounts. Depending on the plan, you may be eligible at 50 or 55 to start adding another $1,000 a year.

In conclusion... if you're in the group of Americans with little to no retirement savings yet, pay attention to the tips we've outlined today. And if you already have several retirement accounts, use this as a refresher to take stock of how you're doing...

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Before you invest for retirement, it's crucial to build your emergency fund. "Around 60% of Americans don't have enough in savings to cover even a $500 emergency," Dave says. Learn how to set up your safety cushion right here: Build This 'Foundation Fund' to Smooth out Life's Surprises.

The money decisions you make today will be with you for a lifetime. So you must choose your retirement account wisely. "If you don't have an IRA or a Roth IRA, you're leaving money on the table," Dave warns... Read more here.

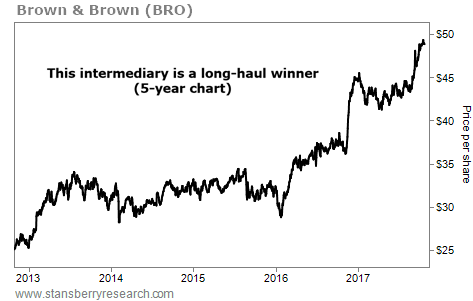

Market NotesTHIS 'MIDDLEMAN' IS QUIETLY MAKING BIG GAINS Today, we look at the benefits of playing the "middleman"...

Insurance companies profit from a rock-solid business model, collecting premiums up front and investing the cash. But often, they have help... Enter the "insurance intermediaries," which act like brokers, connecting folks to insurance products. It's a win-win relationship. And that's why betting on the middleman can be a powerful investing strategy...

Brown & Brown (BRO) is the sixth-largest intermediary in the U.S., offering a slew of insurance-related products and services. The company is enjoying healthy profits, bringing in $1.8 billion in revenue last year – up 6% from 2015. Not only that, but Brown & Brown is using the cash to reward shareholders... It recently raised its dividend for the 24th year in a row.

As you can see in the chart below, shares have soared more than 90% in the past five years. They shot up 31% in the past year alone... and recently hit an all-time high. It goes to show that although supporting players may fly under the radar, they can be stellar long-term investments...

|

Recent Articles

|