Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Steve's note: We're in the "Melt Up" phase of this bull market... And I want you to profit as stocks rise higher than anyone believes possible. But I also want you to prepare for what comes after the Melt Up. My friend and colleague Porter Stansberry, founder of Stansberry Research, believes that when the next crash comes, it could be the most chaotic yet. And in today's essay, he explains the forces that will put it in motion...

What Will Cause the Next CrashBy

Thursday, November 2, 2017

The current bull market is hiding a huge risk...

It's not inflation. It's not accounting fraud. It's not about overvalued stocks.

It's something that's so technical and so difficult to understand that regulators, individual investors, and even the most sophisticated institutions are missing it.

But this risk is HUGE. And it's staring us right in the face...

Today and tomorrow, I am going to tell you about this enormous threat to financial assets and explain why this is what will eventually destroy most of the wealth people believe they now hold in the stock market.

If you want to understand the biggest risk in finance today, you first have to spot the biggest bubble...

Inflation is a poorly understood financial concept. It has nothing to do with price indexes (like the consumer price index or the producer price index). Belief in those measurement tools stems from the 1970s, when inflation flowed into hard assets and commodities.

The big inflation in the last bubble was in residential housing. That should have been obvious to everyone... But it wasn't because we don't call home prices rising much faster than incomes "inflation." We call it the "wealth effect." (Trust me, it's still inflation.)

So... what's the proper definition of inflation?

That's simple: Inflation is the creation of money and credit beyond the savings rate. We have a central bank that creates trillions of dollars of new money with the click of a computer mouse. These funds, produced without any savings, taxes, or increases to productivity, flow through government spending and mortgage finance.

But the government's spending on defense contractors, the medical community, the housing complex, and all of the associated "swamp creatures of the beltway" isn't the real problem. Those are only the first-order impacts of these policies.

You see, the real impact of this new money comes when it enters the banking system. Firms like JPMorgan Chase (JPM) can take $100 million in new government bonds (a reserve asset) and then lend out another $900 million or more in new commercial credit. That's how a real credit bubble is built... by the accumulation of trillions and trillions in new credit.

We've seen this credit inflation occur over and over, ever since we abandoned the gold standard in 1971...

Gold provided a physical limit to credit. Since gold reserves had to be mined, they couldn't merely be wished into existence.

As interest rates have moved lower and lower, the size and scope of the credit bubbles have become bigger and bigger. More borrowing can be financed thanks to the much lower borrowing costs.

Likewise, as interest rates have fallen, vastly more credit could be extended to the most marginal parts of society. Subprime lending only works when institutional credit is available at rates of less than 5% a year.

(Subprime borrowers typically default on 10% or more of these loans, and it's difficult to charge anyone more than 20% a year to borrow money. Ergo, for the business model to work, funding capital must be available at less than 5%, otherwise no operating margin is left to run the business and make a profit.)

Falling interest rates have made each bubble worse than the last...

The commercial real estate bubble of the late 1980s was tiny compared with the tech-stock bubble of 2000... which was less than one-tenth of the size of the mortgage credit bubble of 2007.

With institutional funding rates now close to zero – or in some cases, below zero – the current bubble will be the worst and most disruptive yet.

The next bust will feature far more civil unrest because it has largely been built upon the middle class and the poor.

This credit bubble has seen HUGE amounts of debt added to the accounts of major Western governments (middle-class taxpayers), students (student loans outstanding sit at more than $1.5 trillion), and subprime borrowers (auto loans and credit-card debt each total more than $1 trillion).

As the amount of debt that must be serviced continues to grow much faster than wages, it's simply a matter of time before defaults overwhelm the ability of creditors to pay. At that point, the cycle will reverse... And the crash will come.

None of this is new... or should be news to you...

We've been reporting on these facts for a long time, since we noticed auto lending in particular begin to get out of control back in 2014. Since 2008, the major Western economies have experienced massive inflation. At least $20 trillion has been created in new credit in the U.S. alone, counting new federal debt, new consumer debt, and new corporate debt.

So... in less than 10 years, we've created more new debt than what our entire economy produces in a year. That's an inflation that's bigger than any in our history outside of World War II.

Where has the money and credit gone?

Not into commodities. They've been in a bear market (until recently). Housing prices have rebounded, but they haven't gone crazy. And stocks have certainly gone up, but with a few notable exceptions – like electric-car maker Tesla (TSLA) – they aren't trading at bubble levels.

We have good reason to believe that the bond market (and junk bonds in particular) are trading at highly inflated prices... But that's more a function of the government's manipulation of interest rates than capital flows.

Tomorrow, I'll tell you where the biggest bubble is right now... and what it means for your portfolio.

Good investing,

Porter Stansberry

Further Reading:

"Millions of Americans will soon be calling for it," Porter writes. "Some violently..." Learn why he believes a Debt Jubilee is on the horizon, and how this destructive event is likely to play out, right here: A Lottery That No One Wants to Win.

"Most of America's top companies aren't producing additional cash flows. But they are producing a lot of new debts," Porter says. Read more about these troubled companies, and how to protect your portfolio, right here: The Real Trouble With 'Bizarro Capitalism'.

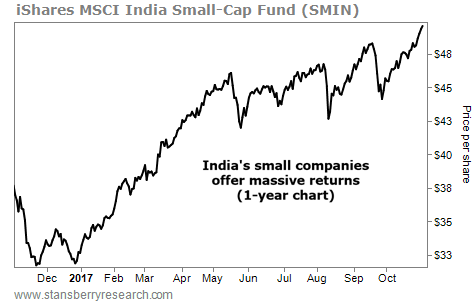

Market NotesTHIS FUND IS A STANDOUT IN EMERGING MARKETS Today, we see small companies benefiting in a high-growth economy...

Longtime readers know emerging markets can offer the kind of massive gains that investors rarely ever find in developed countries. As Steve puts it, "When emerging markets are hot, you simply HAVE to be on board." We can see this at work in India today...

The iShares MSCI India Small-Cap Fund (SMIN) holds 258 small companies in a variety of sectors, including utilities, health care, energy, and financials. These small-cap stocks have a history of soaring hundreds of percent. Meanwhile, India's economy is growing fast... And the Indian government recently said it would inject a record $32 billion into its banks over the next two years. That news sent the country's stocks soaring to record highs.

As you can see in the chart below, shares of SMIN are trading at new 52-week highs after a strong rally in recent months. The fund is up more than 50% since January. Watch for India's developing economy to churn out more gains, especially in these small-cap stocks...

|

Recent Articles

|